The Top Three Drawbacks to Using Target Date Funds

At a high level, two main components impact your retirement savings: 1) How much you are saving and 2) The investments you choose for your money.

While people tend to focus more on the first component, the second one can make an impact to the tune of tens of thousands of dollars over your lifetime. This article will focus on the second component – the investments you choose for your money by peeling back the layers on some of the most popular investments, Target Date Funds (TDFs).

Some of you might have TDFs in your portfolio, some of you might not have heard about them. Here is a general overview of how TDFs work:

Target Date funds make it easy for individuals to select their investments by picking the one closest to the year they will retire (this is why they are so popular in 401k plans). For example, if you hope to retire in 2050, then you could pick the fund marked “Retirement 2050.”

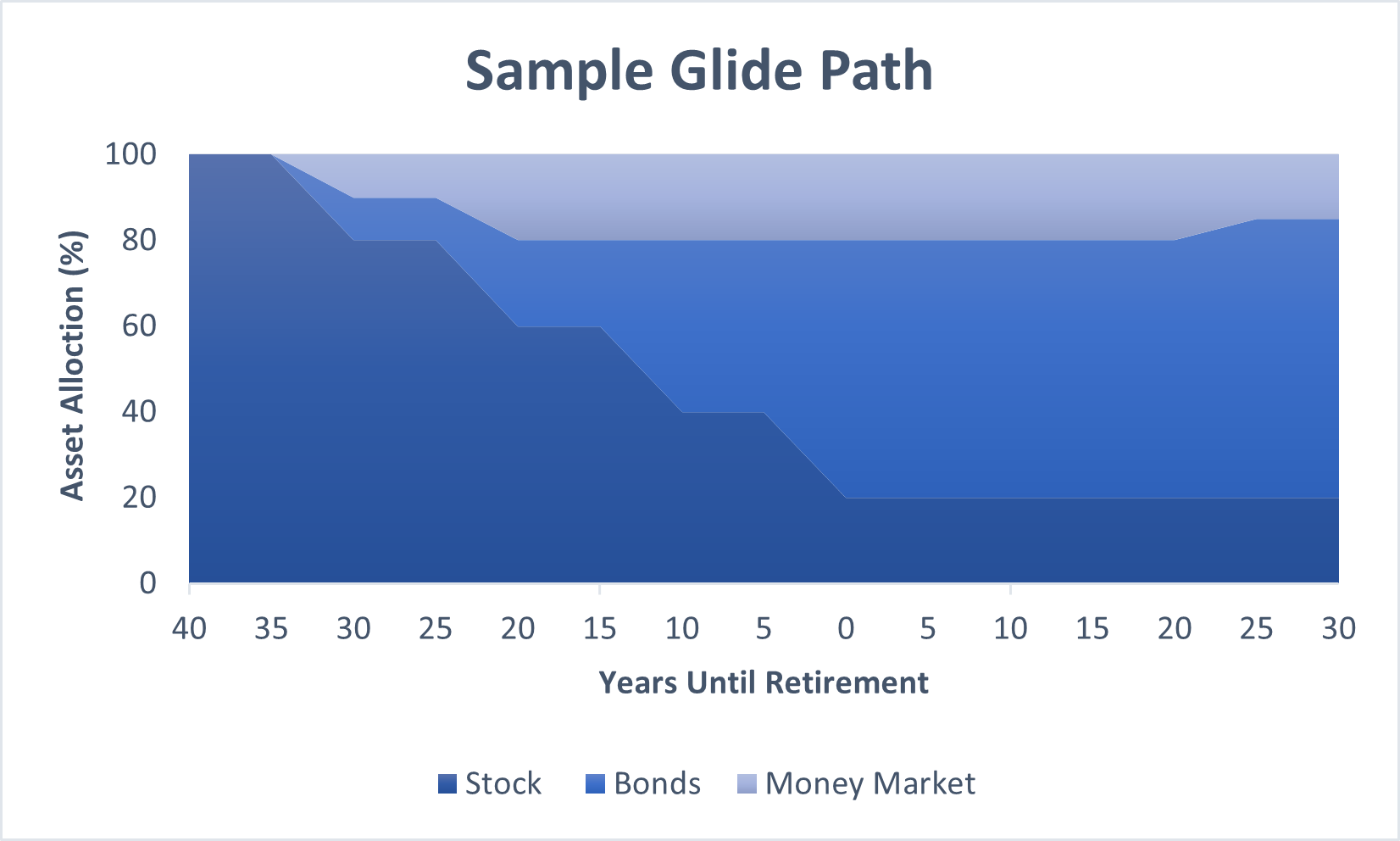

Each of the funds are managed by a portfolio manager (or a team of managers). The managers use a tool called a “glide path” to adjust the underlying mix of investments in that fund.

The glide path helps determine the risk profile of the portfolio, split typically between equities (ex. Stocks and stock funds) and fixed income assets (ex. bond funds and money market funds).

The glide paths typically start out with a larger allocation to equities when participants are farther out from retirement and then slowly take more of a position in fixed income as participants get closer to retirement (see example to the right).

Target date funds gained popularity in the early 2000s. As of 2017, they held over one trillion dollars in assets under management. They are seeming ubiquitous in 401k plans as companies have found participants generally like to “set it and forget it.”

As popular as they have become, as fiduciaries we believe TDFs have some significant drawbacks for plan sponsors and participants. Here are our top drawbacks, especially considering the recent volatility:

TDFs are a “one size fits all” solution.

The main factor the portfolio managers use to determine the assets for each TDF is your time horizon, however it doesn’t account for individual risk tolerance or other special circumstances. As a result, TDFs often have too much or too little exposure in different asset classes for each individual investor.

Two employees could have the same year of retirement – let’s use the year 2050 – but entirely different risk tolerances and circumstances. One could be much more conservative and interested in preserving their capital, while another is wanting to achieve higher returns and is willing to take on more risk. Additionally, each person could have other assets to consider (i.e. one has a spouse with assets or an outside brokerage account or stock options from a previous employer). The glide path doesn’t take your specific needs into account.

TDFs may charge higher fees.

All funds (mutual funds, bond funds) have what is known as an “expense ratio” – or what it costs to participate in the fund. The goal is to keep the expense ratio as low as possible (higher expense ratio = more fees from your account rather than in your pocket). Not only might the Target Date Fund not best meet your needs, but their fees are typically higher than what we like to see clients pay.

Here is an example: American Funds 2060 Target Date Retirement Fund (AANTX) has an expense ratio of .72% (this one TDF of many we could choose from - we are not picking on American Funds!). The asset allocation is as follows:

US Equities: 59%

Non-US Equities: 26%

US Bonds: 7.5%

Non-US Bonds: 1.3%

Cash: 6%

If you wanted to roughly mirror those allocation, you could invest in the following (this is for illustrative purposes only):

US Equities: Fidelity Total Stock Market 0.015%

Non-US Equities: Vanguard European Stock Index Fund: .13%

US Bonds: Vanguard Total Bond Market 0.05%

Non-US Bonds: Vanguard Total International Bond .11%

Cash: Vanguard Money Market .011%

The overall expense ratio for this example portfolio is .13% compared to the American funds 2060 Fund with the expense ratio of .72% - so, a very similar asset allocation for a fraction of the expense. Over the course of your investment, this cost could add up significantly.

3. In a rising interest rate environment, most if not all TDFs did not offer capital protection to near-retirees.

“2022 was a rough year for near-retirees in Target Date Funds...those with a 2025 vintage saw median total returns of -15.4%.”

As noted in Investment News Magazine’s article “2022 was a Rough Year for Near-retirees in Target Date Funds”, it was a detrimental time to be close to retirement and invested in TDF. Specifically, “those with a 2025 Vintage saw median total returns of -15.4%, only slightly higher than the median of -18.3 for 2055 funds.”

Bonds are generally thought of as “safe assets” – or low risk for a comparatively lower return. The glide paths of most TDFs leaned heavily towards bonds for those close to retirement (see the example above) to help preserve retirees capital.

However, bond prices decline in the rare scenario when the Fed quickly raises rates to combat something in the economy, like inflation. The last notable time this occurred was the 1980s, but it occurred again over the past year as the Fed raised rates. Most Target Date Funds did not move money out of bonds and into other asset classes, like cash, to preserve near-retirees capital and the funds suffered larger-than-expected losses.

Overall, TDFs make it easy for participants to choose an investment – and that solves a huge problem for participants. However, as fiduciaries, we always point out the shortcomings of these funds with our wealth management clients and help them choose the lowest cost investments that both meet their time horizon AND risk tolerance as well as their personal circumstances.

For our 401k and 403b participants, we offer Target Risk funds (more on those here) created from low-cost index funds and ETFs rather than Target Date funds. While it requires participants to understand their time horizon and risk tolerance, we guide them through this during the enrollment process, ultimately landing them in funds tailored to their unique investing needs.

Please reach out if you have any questions about your own portfolio!